》View SMM Metal Prices, Data, and Market Analysis

》Subscribe to View Historical Price Trends of SMM Spot Metals

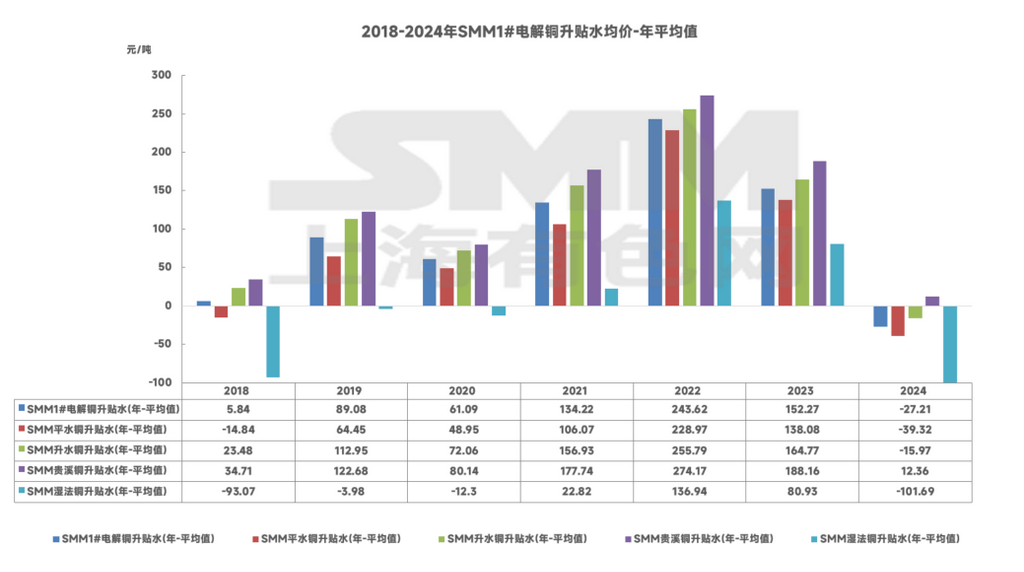

The last trading day of 2024 ended on December 31, with SHFE spot copper closing at an average discount for the year, breaking the premium trend of the past seven years.

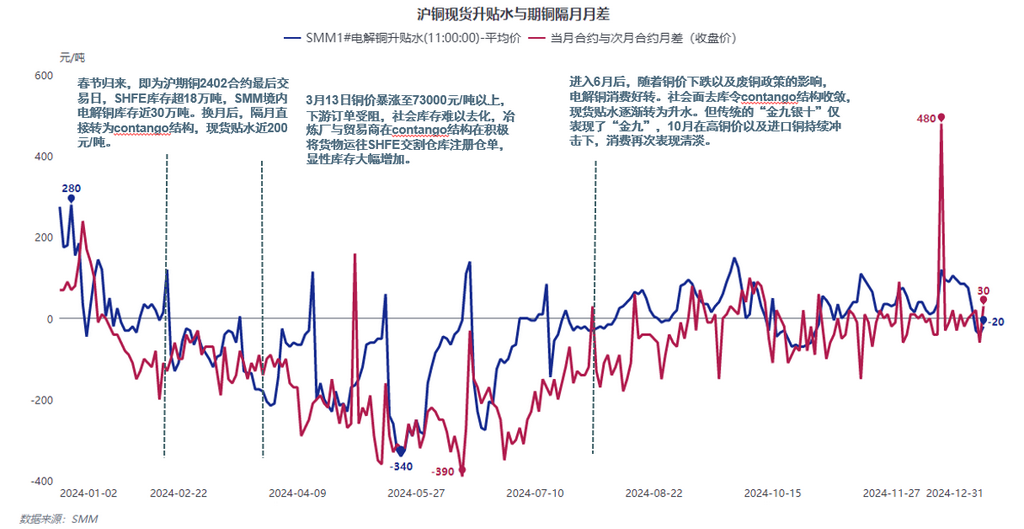

Looking back at 2024, since mid-March, copper prices began to rise due to supply-side factors. Under the influence of high copper prices and high inventory, spot copper consistently traded at a discount to futures. Both SHFE and LME exhibited a contango structure. After the Chinese New Year, traditional borrow operations were trapped, and copper prices unexpectedly broke historical highs, causing downstream production to halt temporarily. Against the backdrop of high premiums for fixed long-term contracts in 2024, downstream enterprises faced significant losses in spot order procurement compared to long-term contracts, leading to defaults among end-users and processing material sectors.

From June onwards, copper prices gradually declined, the price difference between primary metal and scrap narrowed, and with the impact of "reverse invoicing" and the Fair Competition Review Regulations on secondary copper, copper cathode consumption was boosted. Spot copper finally transitioned from sustained discounts to premiums, but the premium of 100 yuan/mt was difficult to maintain. The persistent contango structure in distant months failed to provide hope for a significant rise in spot premiums. However, in the second half of the year, the market gradually accepted copper price fluctuations in the range of 73,000-76,000 yuan/mt, with spot premiums and discounts relatively stabilizing.

With the determination of processing fees at the mine end in early December, negotiations for domestic copper cathode long-term contracts were also initiated. It is reported that the fixed premium quotations for copper cathode by smelters in 2025 did not significantly loosen despite the annual average discount in 2024, with most companies only reducing their quotes by 20-40 yuan/mt compared to 2024. If the proportion of fixed long-term contracts signed by downstream enterprises decreases, the activity of spot orders in 2025 is expected to increase significantly. What sparks will the spot market ignite?

》View SMM Metal Industry Chain Database